Mortgage Woes

Surging inflation and unemployment in the 1970s put pressure on the economy, and by 1980 it had landed in recession. Mortgages became a huge problem; interest rates reached nearly 20%, and most people couldn’t afford to buy homes. Payments were so high for those who did buy homes that they often fell behind. Unemployment surged at the same time, and foreclosures rose while home sales crashed.

Things began to turn around late in 1982 when the government lowered interest rates. People scrambled to refinance their home loans. When home sales also improved, mortgage lending took off.

In April 1984, Lakeland Financial Corporation formed Lakeland Mortgage Corporation to write and resell home mortgages. Based in Carmel, Indiana, Lakeland Mortgage opened with five people on staff. Within months, offices were added in Fort Wayne, Lafayette, Anderson and South Bend, and together they employed more than 30 people.

In April 1984, Lakeland Financial Corporation formed Lakeland Mortgage Corporation to write and resell home mortgages. Based in Carmel, Indiana, Lakeland Mortgage opened with five people on staff. Within months, offices were added in Fort Wayne, Lafayette, Anderson and South Bend, and together they employed more than 30 people.

Business took off right away. At one point, Lakeland Mortgage exceeded its goals by 224%, and executives projected more than $125 million in business during the first full year of operation.

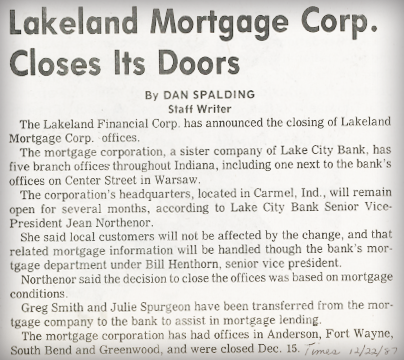

But the market changed again. Conditions at home and across the country got worse, and long-term mortgage rates started to rise again. Overall mortgage sales to the secondary market dropped from roughly 70% to just 30% in a single year. Lakeland Mortgage found itself struggling, and as quickly as it had opened, the company shut down. By December 1987, Lakeland Mortgage had closed its doors.

But the market changed again. Conditions at home and across the country got worse, and long-term mortgage rates started to rise again. Overall mortgage sales to the secondary market dropped from roughly 70% to just 30% in a single year. Lakeland Mortgage found itself struggling, and as quickly as it had opened, the company shut down. By December 1987, Lakeland Mortgage had closed its doors.

All customer information was transferred to the bank’s existing mortgage department with no loss of service.